.png)

High-income earner? Get ahead with strategic tax planning before Q3. Discover key moves to reduce your tax burden, maximize deductions, and stay IRS-compliant.

For high-income earners, tax planning is not just a year-end scramble—it’s a strategic, year-round effort. As we move through Q3 of 2025, now is the time to get proactive. Whether you’re a business owner, executive, investor, or someone earning well into six or seven figures, your tax decisions in the next few months could mean the difference between thousands saved—or lost—on your next return.

Here’s what high-income earners should focus on before Q3 ends, with 2025-specific tips, IRS guidance, and actionable strategies.

High-income taxpayers often don’t have enough taxes withheld from their paycheck—or they have multiple income streams like investments, self-employment, or rental income.

If your adjusted gross income (AGI) exceeds $150,000 ($75,000 if married filing separately), the IRS requires you to pay at least 110% of your prior year’s tax liability or 90% of your current year’s tax, whichever is less, to avoid penalties.

📅 Action Item: Evaluate your Form 1040-ES quarterly payments. The Q3 payment is due September 15, 2025.

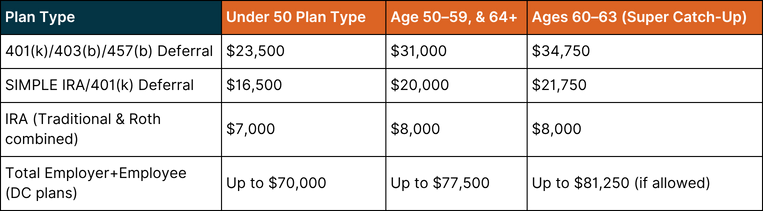

Tax-advantaged retirement accounts are one of the best tools to reduce taxable income—especially at high income levels.

For 2025, here are the updated IRS-confirmed limits:

💡 Tip: If your income is too high to contribute directly to a Roth IRA (over $240,000 MFJ), consider a Backdoor Roth IRA strategy—just be mindful of the pro-rata rule.

🔗 IRS: Retirement Plan Contribution Limits

If you’ve had a volatile investment year, now is the time to harvest capital losses to offset gains—or even up to $3,000 of ordinary income.

Conversely, if you’re in a lower-income year (say, due to a gap between jobs or a business loss), consider realizing long-term capital gains at the 0% or 15% rate—especially before Q4 volatility hits.

📈 Example: Selling underperforming stocks now and repurchasing similar (not “substantially identical”) investments after 30 days can preserve your portfolio while locking in tax savings.

🔗 IRS: Tax Loss Harvesting Rules

If you itemize deductions, charitable giving is still one of the most powerful tools for reducing taxable income.

💡 Tip: High earners often exceed the standard deduction, which in 2025 is $30,000 MFJ / $15,000 Single (or $31,500 MFJ / $15,750 Single after the OBBB increase), so maximizing deductions through planned giving can be highly effective.

🔗 IRS: Charitable Contribution Deductions

Earn over $200,000 ($250,000 MFJ)? You’re subject to the 3.8% NIIT on:

📊 Action Step: Review your portfolio and consider asset placement (taxable vs. tax-advantaged accounts), and investment types (dividend-heavy vs. growth).

🔗 IRS: Net Investment Income Tax

The Alternative Minimum Tax (AMT) still trips up many high earners. It removes deductions like:

🛡️ Tip: Avoid large ISO exercises without tax planning. Coordinate with a tax advisor to time exercises, deductions, and capital gains wisely.

Business owners, freelancers, and high-income consultants should revisit income timing, deductions, and entity structure before Q4.

📂 Example: A married consultant earning $400,000 from an S-Corp may benefit from salary/dividend restructuring, maximizing solo 401(k) contributions, and QBI deduction optimization.

🔗 IRS: QBI Deduction Info

If you’re in a high-tax state (like California, New York, or New Jersey), now is the time to explore:

📌 Note: The SALT deduction is still capped at $40,000 for 2025 (pending congressional changes).

🔗 IRS: State and Local Tax Deduction Limit

With the lifetime estate and gift tax exemption at $13.99 million per person in 2025 (set to sunset in 2026), wealthy families should consider locking in today’s high limits.

🔗 IRS: Estate and Gift Tax Limits

Tax planning isn’t just about saving money—it’s about aligning your financial goals, protecting your wealth, and staying ahead of costly surprises. As a high-income earner, the tax code can be both a minefield and a toolkit. You just need the right strategy—and the right guide.

At Vincere Tax, we specialize in proactive tax planning for high-income individuals and business owners. Let’s make sure your Q3 tax strategy sets you up for a successful 2025.

📞 Need a mid-year tax check-in? Book a strategy call with us today »

Maximize retirement plans (including backdoor Roth), harvest losses, leverage charitable giving (DAFs or appreciated stock), and explore entity restructuring if self-employed.

Yes, for workplace plans like 401(k)s, you can contribute through December 31, 2025. IRAs can be funded up to the April 2026 filing deadline.

Limit preference items like ISO exercises and manage SALT deductions. A tax projection can help identify exposure early.

Yes, appreciated stock avoids capital gains and gives you a full-value deduction if held over a year.

Document your domicile change carefully, avoid part-year residency pitfalls, and consider timing large income events post-move.

Let Vincere Tax be your trusted partner in navigating the complex tax landscape. It’s not just about tax season—it’s about making every season count.

Being audited is comparable to being struck by lightning. You don't want to practice pole vaulting in a thunderstorm just because it's unlikely. Making sure your books are accurate and your taxes are filed on time is one of the best ways to keep your head down during tax season. Check out Vincere's take on tax season!

This post is just for informational purposes and is not meant to be legal, business, or tax advice. Regarding the matters discussed in this post, each individual should consult his or her own attorney, business advisor, or tax advisor. Vincere accepts no responsibility for actions taken in reliance on the information contained in this document.

For business tax planning articles, our tax resources provides valuable insights into how you can reduce your tax liability now, and in the future.

.png)

At Vincere Tax, we've got the skills and know-how to craft a unique, tailored plan just for you. Trust us – we've got the expertise to make it happen!

Speak with an expert Website Terms.png)

.png)

.png)

Copyright © 2025 Vincere Tax| All Rights Reserved

Privacy Policy

.png)