.png)

Changed jobs in 2025? Here’s how it impacts your taxes—W-2s, retirement, healthcare, and more. Learn what to expect and how to stay ahead

Changing jobs can be exciting—new opportunities, better pay, maybe even a relocation. But a job change also comes with a ripple effect on your taxes. Whether you switched employers for career growth or were part of a layoff, the IRS still wants its share. Knowing how a job switch affects your 2025 tax return can help you avoid surprises—and even save money.

Here’s what you need to know.

When you change employers, each one is required to send you a Form W-2 by January 31, 2026. You’ll need all of them when filing your 2025 return. If you had more than one job, your income from each employer adds together, potentially pushing you into a higher tax bracket.

Let’s say your first job paid you $80,000 and your second job paid $50,000. Combined, your 2025 income is $130,000, placing you in a higher marginal tax bracket. If each employer only withheld taxes based on your income with them, your total withholding might be too low—resulting in a tax bill when you file.

📌 Pro Tip: Use the IRS Tax Withholding Estimator when you change jobs to ensure the correct amount is withheld from your paychecks.

Also, double-check that each W-2 is accurate. Errors in reported income or withheld taxes can delay your refund or trigger audits.

The Social Security wage base for 2025 is $176,100. If you earned over this amount across multiple jobs, and each employer withheld Social Security tax up to the full wage base, you may have overpaid.

You’ll get the excess Social Security tax back as a credit on your tax return when you file Form 1040. The IRS auto-calculates this when you report your W-2s.

Each employer calculates Social Security withholding independently. There’s no real-time system that tells them you’ve already maxed out elsewhere.

⚠️ Heads-Up: Medicare tax doesn’t have a wage cap. In fact, if you earn more than $200,000 ($250,000 for married couples), you may be subject to the 0.9% Additional Medicare Tax.

If your new job took you to another state—or you worked remotely in a different state—you could face multi-state tax filings. Each state has different residency rules, and some may want to tax part of your income.

🏡 Example: You lived in Illinois and switched to a remote job based in California. If you spent time working in both states, both may claim you owe them income taxes.

✍️ Tip: Keep detailed records of where you physically worked and when. Use a calendar, time-tracking app, or expense log.

If you had a gap between jobs and received unemployment compensation, remember: these benefits are fully taxable at the federal level.

📃 You should receive a Form 1099-G from your state showing the total unemployment benefits you received in 2025.

💡 Tip: Many people forget to withhold taxes from unemployment checks. If you didn’t, you might owe money when you file.

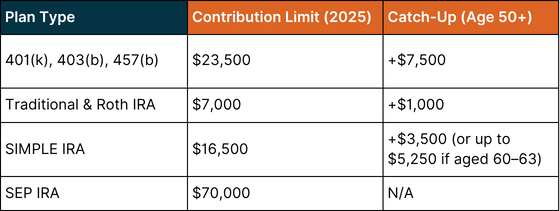

When changing jobs, your retirement savings could take a temporary hit—especially if you weren’t eligible to contribute to a new 401(k) plan right away. However, you may still be able to maximize contributions in other ways.

▶️ Don’t Forget to Rollover:

If you had a 401(k) with your old employer, consider rolling it into an IRA or your new 401(k) to avoid taxes or penalties. Use a direct rollover to stay tax-free.

📅 If you had a gap in coverage, consider contributing to an IRA on your own.

Switching jobs often means a change in health insurance. If you had a Health Savings Account (HSA), here’s what to keep in mind:

📄 Important: If your previous employer contributed to your HSA and you also did, check that you didn’t exceed the annual limit. Excess contributions are subject to a 6% penalty.

If you received equity compensation at your previous or new job—like RSUs (restricted stock units), stock options, or participated in an ESPP (employee stock purchase plan)—these have unique tax implications.

💡 Tip: If your RSUs vested while you were between jobs or before joining a new one, be sure to account for the income in your year-end tax planning.

📘 Learn more on IRS Publication 525 for how different types of compensation are taxed.

Job transitions often include lump sum payments like signing bonuses, severance packages, or accrued vacation payouts. These are all taxable income and may be taxed at a higher rate depending on your total income for the year.

💸 Severance & PTO payouts are typically included in your final paycheck and subject to federal income tax, Social Security, and Medicare tax.

💡 Signing bonuses may be subject to clawback if you leave your new job too soon—read the fine print!

Not all benefits travel with you. If you leave a job before you're fully vested in your employer 401(k) match, you may forfeit some of that money.

🕵️♀️ Also double-check:

After switching jobs, file a new Form W-4 with your employer. Many people skip this step—and it can lead to under-withholding (you owe the IRS) or over-withholding (you get a smaller paycheck all year).

🔄 Use the IRS Tax Withholding Estimator to fine-tune your paycheck

💡 Tip: If your new job pays more or you're combining incomes from multiple jobs (or a spouse), adjust your W-4 to avoid a surprise tax bill next April.

Changing jobs can reset a lot of financial gears—from how much tax is withheld to whether you're contributing enough to your future retirement. But being proactive—tracking your income, reviewing your benefits, updating your W-4, and watching for multi-state or benefit complications—can prevent an unwelcome tax bill in 2026.

🧠 Consider scheduling a mid-year tax planning session with a tax advisor at Vincere Tax. We’ll help you:

✅ Avoid underpayment penalties

✅ Maximize new benefits

✅ Rollover old retirement plans

✅ Identify state filing requirements

✅ And prepare for equity or bonus taxes

Maybe. If you moved during the year or earned income in multiple states, you may need to file part-year resident returns or nonresident returns depending on state laws.

It’s treated as ordinary income and subject to regular payroll tax withholding. But it can bump up your bracket depending on timing.

Not anymore. The deduction for unreimbursed employee expenses, including job hunting costs, was suspended by the Tax Cuts and Jobs Act through 2025.

Contact your old employer for a replacement. If you can’t get one, file with Form 4852, a substitute W-2.

Yes, as long as you had earned income during the year and meet income limits. In 2025, you can contribute up to $7,000 (or $8,000 if age 50+).

Being audited is comparable to being struck by lightning. You don't want to practice pole vaulting in a thunderstorm just because it's unlikely. Making sure your books are accurate and your taxes are filed on time is one of the best ways to keep your head down during tax season. Check out Vincere's take on tax season!

This post is just for informational purposes and is not meant to be legal, business, or tax advice. Regarding the matters discussed in this post, each individual should consult his or her own attorney, business advisor, or tax advisor. Vincere accepts no responsibility for actions taken in reliance on the information contained in this document.

For business tax planning articles, our tax resources provides valuable insights into how you can reduce your tax liability now, and in the future.

.png)

At Vincere Tax, we've got the skills and know-how to craft a unique, tailored plan just for you. Trust us – we've got the expertise to make it happen!

Speak with an expert Website Terms.png)

.png)

.png)

Copyright © 2025 Vincere Tax| All Rights Reserved

Privacy Policy

.png)