.png)

Mid-year is the perfect time to optimize your 2025 retirement contributions. Learn the latest IRS limits, super catch-up rules, and Roth strategies in this expert guide.

.png)

As we enter the second half of 2025, now is the ideal time to assess your retirement savings strategy. With updated IRS contribution limits and new provisions from SECURE 2.0 in effect, reviewing your contributions now can help you avoid tax-time surprises and capitalize on powerful saving opportunities.

At Vincere Tax, we believe financial success begins with year-round planning—not scrambling in April. This mid-year guide walks you through 2025’s contribution limits, updated tax strategies, and smart moves to make now that will pay off for decades to come.

A Q3 retirement review gives you time and flexibility to:

📅 Mid-year planning gives you a second chance to ensure you’re not leaving tax advantages or employer matches on the table.

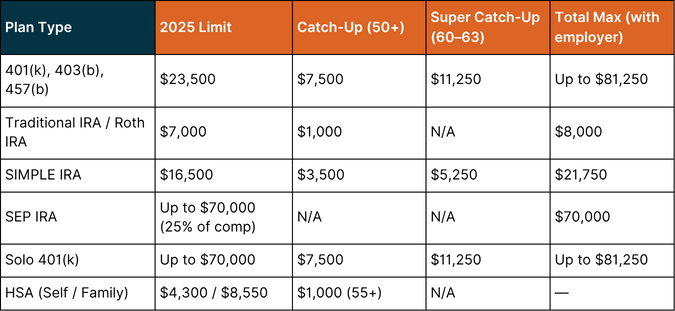

Several retirement savings limits increased in 2025 due to inflation adjustments and expanded catch-up rules under SECURE 2.0:

As your income or tax bracket changes, the ideal retirement strategy may shift. For instance:

📌 Ask yourself:

“Do I believe tax rates will be higher or lower when I retire?”

If higher → Roth

If lower → Traditional

Tax laws are in flux, and many believe rates could rise after 2026 when current cuts expire. This makes Roth contributions attractive in 2025, especially for younger savers or early retirees.

For married couples with two incomes, mid-year is the perfect time to coordinate and maximize contributions across plans:

💡 Tip: One partner can use Roth while the other uses Traditional—diversifying tax outcomes in retirement.

Many high earners try to max out early in the year. That’s fine—unless your employer match is based on per-pay-period contributions. In that case, front-loading could cost you thousands in lost free money.

Starting in 2025, savers aged 60–63 are eligible for “super catch-up” contributions to employer plans:

📌 This is a critical tax-saving opportunity during peak earning years. But not all plans have adopted this provision yet, so verify with your HR or benefits department.

Even if you max out a workplace plan, you might still be eligible for:

Roth IRA income phase-outs (2025):

Whether you’re a consultant, freelancer, or side hustler, consider:

Tip: Use both employer and employee roles strategically to maximize tax deferral and flexibility.

Health Savings Accounts (HSAs) are the most tax-advantaged account available—and most underutilized.

Use them to:

This is the ultimate Roth strategy if your plan allows:

If your 401(k) permits after-tax contributions and in-service withdrawals or in-plan Roth conversions, this strategy can supercharge your tax-free retirement growth.

Maya, 59, is self-employed with $220,000 in net income. In July 2025, she hadn’t contributed anything yet. After meeting with Vincere Tax:

✅ Outcome: She reduced her 2025 taxable income by over $55,000 and set aside over $67,000 for retirement—in just half a year.

We specialize in helping:

Our mid-year strategy session includes:

✅ Contribution and deduction optimization

✅ Traditional vs. Roth comparison

✅ Backdoor & Mega Backdoor Roth execution

✅ SEP & Solo 401(k) plan design

✅ Year-end tax liability projections

📅 Book your mid-year strategy call with Vincere Tax now. Why wait until December?

The second half of the year is your final chance to:

Whether you're employed, self-employed, or somewhere in between—you still have time to make 2025 your best financial year yet.

🔑 Let Vincere Tax help you retire smarter, sooner, and with less stress. Your future self will thank you.

You may face a 6% penalty on excess IRA contributions unless corrected by the tax deadline. Work with a tax pro to fix it.

Yes—but your IRA deduction may be limited if you’re covered by a workplace plan and over the income limit.

Yes, but improper execution can trigger taxes. Vincere Tax helps clients do it right—step by step.

December 31, 2025 for 2025 contributions. (Funding can happen later.)

It depends on your current vs. future tax bracket and whether you want to avoid RMDs. A mid-year tax review can help decide.

Being audited is comparable to being struck by lightning. You don't want to practice pole vaulting in a thunderstorm just because it's unlikely. Making sure your books are accurate and your taxes are filed on time is one of the best ways to keep your head down during tax season. Check out Vincere's take on tax season!

This post is just for informational purposes and is not meant to be legal, business, or tax advice. Regarding the matters discussed in this post, each individual should consult his or her own attorney, business advisor, or tax advisor. Vincere accepts no responsibility for actions taken in reliance on the information contained in this document.

For business tax planning articles, our tax resources provides valuable insights into how you can reduce your tax liability now, and in the future.

.png)

At Vincere Tax, we've got the skills and know-how to craft a unique, tailored plan just for you. Trust us – we've got the expertise to make it happen!

Speak with an expert Website Terms.png)

.png)

.png)

Copyright © 2025 Vincere Tax| All Rights Reserved

Privacy Policy

.png)