Compare Solo 401k vs SEP IRA in 2026. Learn contribution limits, tax benefits, and which retirement plan is best for self-employed professionals and business owners.

For entrepreneurs, freelancers, and small business owners, retirement planning isn’t just about saving for the future — it’s also one of the most powerful tax planning strategies available.

Choosing the right retirement plan can significantly reduce your taxable income while helping you build long-term wealth. But with multiple options available, many business owners ask the same question:

Each plan offers different contribution limits, flexibility, and tax advantages. The best option depends on factors such as your income level, business structure, number of employees, and retirement goals.

In this guide, we’ll compare the Solo 401k vs SEP IRA 2026, explain how Defined Benefit Plans work, and help you determine which retirement strategy may be right for your business.

Watch this video:🚀 Solo 401k, SEP IRA, or Defined Benefit? Find Your Perfect Plan

Many business owners reinvest profits back into their companies. While growing a business is important, relying solely on a future exit for retirement can be risky.

Strategic retirement planning offers several key benefits.

Most retirement contributions are tax-deductible, reducing taxable income for the year.

Investments inside retirement accounts grow tax-free until withdrawal, allowing compounding to accelerate wealth.

Many retirement plans offer strong creditor protection under federal law.

Consistent contributions over time can build substantial retirement wealth.

🤝 If you’re a business owner looking to reduce taxes this year, you may also want to explore year-end tax strategies for entrepreneurs.

The Solo 401(k) is designed specifically for self-employed individuals or business owners with no full-time employees(other than a spouse).

Because it allows you to contribute as both an employee and employer, it offers one of the highest retirement contribution limits available. According to the Internal Revenue Service, Solo 401k contribution limits are adjusted periodically for inflation.

With a Solo 401k, contributions come from two sources:

You contribute part of your salary just like an employee would in a traditional 401(k).

Your business contributes an additional percentage of profits.

This dual structure allows self-employed professionals to maximize retirement contributions much faster than traditional IRAs.

For the 2026 tax year, limits include:

• Employee contribution: $24,500

• Employer contribution: Up to 25% of compensation

• Total contribution limit: $72,000

💡If you are age 50 or older, you may contribute an additional $8,000 catch-up contribution.

The combination of employee and employer contributions allows aggressive retirement savings.

Some Solo 401k plans allow Roth contributions, which provide tax-free withdrawals in retirement.

Participants may borrow up to $50,000 or 50% of their account balance depending on plan rules.

If your spouse works in the business, they can contribute as well, effectively doubling retirement savings potential.

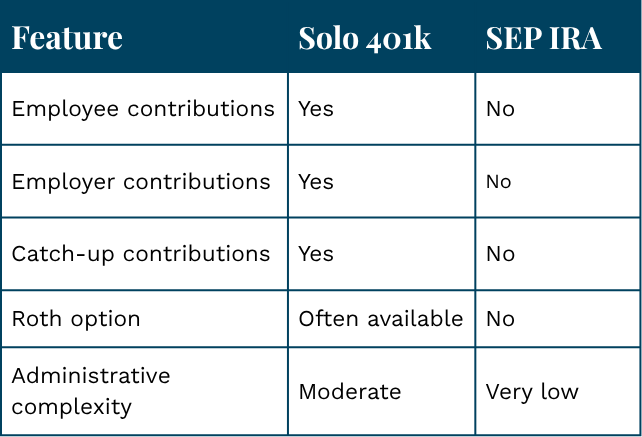

When comparing Solo 401k vs SEP IRA 2026, several differences stand out.

In general:

• Solo 401k plans offer greater flexibility and higher contribution potential.

• SEP IRAs offer simplicity and minimal administration.

Before selecting a retirement plan, consider the following:

Certain plans require contributions for employees as well.

Higher-income individuals may benefit from higher contribution limits.

Older professionals often benefit more from Defined Benefit Plans.

Plans with mandatory contributions may not work well for businesses with fluctuating revenue.

Choosing the right retirement plan can dramatically impact both your tax liability and long-term financial security.

At Vincere Tax, we help entrepreneurs and business owners develop tax-efficient retirement strategies.

Our services include:

• Retirement tax planning

• Solo 401k strategy and setup

• SEP IRA planning

• Defined Benefit Plan strategies

• Year-end tax optimization

Understanding the differences between Solo 401k vs SEP IRA 2026 can help business owners maximize retirement contributions while reducing taxes.

Meanwhile, the Defined Benefit Plan allows high-income professionals to make extremely large tax-deductible contributions. With proper planning, the right retirement strategy can help you reduce taxes today while building long-term financial security.

The main difference between a Solo 401(k) and a SEP IRA is how contributions are made. A Solo 401k allows both employee and employer contributions, while a SEP IRA only allows employer contributions. This means Solo 401k plans often allow higher contributions at lower income levels.

For the 2026 tax year, the Solo 401k contribution limit is up to $72,000 total, combining employee and employer contributions. Individuals age 50 or older may also qualify for an additional catch-up contribution, allowing even higher retirement savings.

A Solo 401k is designed for self-employed individuals or business owners with no full-time employees other than a spouse. Freelancers, consultants, independent contractors, and single-owner businesses commonly use this retirement plan.

A SEP IRA can work well for small businesses with employees because it is easy to set up and has minimal administrative requirements. However, employers must contribute the same percentage of compensation to all eligible employees, which can make it more expensive as a business grows.

High-income business owners who want to contribute more than the limits allowed by a Solo 401k or SEP IRA may benefit from a Defined Benefit Plan. These plans can allow very large tax-deductible contributions, sometimes exceeding six figures annually depending on age and income.

Being audited is comparable to being struck by lightning. You don't want to practice pole vaulting in a thunderstorm just because it's unlikely. Making sure your books are accurate and your taxes are filed on time is one of the best ways to keep your head down during tax season. Check out Vincere's take on tax season!

This post is just for informational purposes and is not meant to be legal, business, or tax advice. Regarding the matters discussed in this post, each individual should consult his or her own attorney, business advisor, or tax advisor. Vincere accepts no responsibility for actions taken in reliance on the information contained in this document.

For business tax planning articles, our tax resources provides valuable insights into how you can reduce your tax liability now, and in the future.

.png)

At Vincere Tax, we've got the skills and know-how to craft a unique, tailored plan just for you. Trust us – we've got the expertise to make it happen!

Speak with an expert Website Terms.png)

.png)

.png)

Copyright © 2025 Vincere Tax| All Rights Reserved

Privacy Policy