.png)

Missing the September 16 estimated tax deadline could mean costly penalties. Here’s how to prepare, calculate what you owe, and avoid common mistakes—whether you’re self-employed or earn side income in 2025.

If you're self-employed, a freelancer, a gig worker, or you earn investment income, you don’t have an employer withholding taxes from your paycheck. That’s where estimated taxes come in. Instead of waiting until April, the IRS requires you to pay taxes throughout the year in four quarterly installments.

📅 The upcoming Q3 estimated tax payment is due on September 16, 2025, and skipping it can lead to underpayment penalties—even if you plan to pay in full later.

At Vincere Tax, we help clients navigate the complexity of quarterly taxes with clarity. Whether this is your first time making an estimated payment or you’ve done this before, here's how to prepare with confidence.

You’re generally required to make estimated tax payments if:

Even if you have a W-2 job, side income may still trigger the need for estimated taxes.

👉 Example: If you freelance on weekends and expect to earn $15,000 this year in side income—with no taxes withheld—you’ll likely need to pay estimated taxes to avoid underpayment penalties.

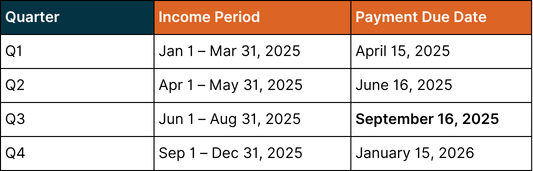

Here are the four IRS due dates for the 2025 tax year:

📅 If the due date falls on a weekend or holiday, the deadline shifts to the next business day.

Use your year-to-date earnings, invoices, and investment statements to project your total income for the year.

Tools like accounting software (e.g., QuickBooks, Wave) or spreadsheets can help organize this.

For 2025, here are the federal income tax brackets (for illustrative purposes):

You’ll also owe 15.3% in self-employment tax if you’re earning from freelance or gig work. This includes:

High earners may owe an additional 0.9% Medicare surtax above $200,000 (single) or $250,000 (MFJ).

👉 Use the IRS Form 1040-ES worksheet

Lower your estimated tax by accounting for:

Once you estimate your total tax liability, divide it into four equal payments—unless your income is seasonal or irregular, in which case the annualized income method may be more accurate.

👉 Example:You estimate $12,000 in total tax owed. You’ve already paid $4,000 in Q1 and Q2 combined. That leaves $8,000. Split between Q3 and Q4, you’ll owe $4,000 each for September 16 and January 15.

You can pay online at IRS Direct Pay, by debit/credit card, or through the Electronic Federal Tax Payment System (EFTPS).

💡 Tip: If you expect to owe state estimated taxes (like in California or New York), check your state’s website for separate deadlines and payment portals.

If you miss a payment or underpay, the IRS may charge underpayment penalties and interest, even if you pay everything by April 2026.

If your income spikes mid-year, your earlier estimates may be too low. Adjust Q3 and Q4 payments accordingly.

If you earn side income, your employer’s withholding likely won’t be enough.

The IRS still charges penalties even if you pay the full amount by April.

Make sure to use the correct quarter and year when making payments—especially through EFTPS or IRS Direct Pay.

Want to reduce your Q3 estimated payment? Here are a few strategies:

Once Q3 is out of the way, it’s time to look ahead. The final estimated tax payment is due January 15, 2026, covering September through December.

If you earn income without withholding, the September 16 estimated tax deadline is too important to ignore. Getting it right means avoiding penalties, reducing surprises in April, and keeping your financial health on track.

Estimated taxes don’t have to be overwhelming. At Vincere Tax, we help self-employed individuals, business owners, and investors stay on top of quarterly deadlines with proactive strategies and expert support.

Need help calculating or submitting your September 16 payment?

📞 Book a free consultation with Vincere Tax today.

Let’s take the stress out of tax season—one quarter at a time.

You’ll receive a refund when you file your 2025 tax return.

Yes—if you have substantial side income or investment gains not covered by withholding.

Yes! The IRS doesn’t require quarterly payments to be one lump sum—you can break them up monthly as long as the total is paid by the deadline.

Use the annualized income installment method on IRS Form 2210 to match your payments to actual income earned.

Most likely, yes. Each state has different rules. Check your state’s Department of Revenue or talk to Vincere Tax for guidance.

Being audited is comparable to being struck by lightning. You don't want to practice pole vaulting in a thunderstorm just because it's unlikely. Making sure your books are accurate and your taxes are filed on time is one of the best ways to keep your head down during tax season. Check out Vincere's take on tax season!

This post is just for informational purposes and is not meant to be legal, business, or tax advice. Regarding the matters discussed in this post, each individual should consult his or her own attorney, business advisor, or tax advisor. Vincere accepts no responsibility for actions taken in reliance on the information contained in this document.

For business tax planning articles, our tax resources provides valuable insights into how you can reduce your tax liability now, and in the future.

.png)

At Vincere Tax, we've got the skills and know-how to craft a unique, tailored plan just for you. Trust us – we've got the expertise to make it happen!

Speak with an expert Website Terms.png)

.png)

.png)

Copyright © 2025 Vincere Tax| All Rights Reserved

Privacy Policy