Discover how tax brackets changed from 2025 to 2026, what the updates mean for your income, and smart strategies to plan ahead.

For both tax years, the federal income tax system retains seven marginal tax rates: 10%, 12%, 22%, 24%, 32%, 35%, and 37%. These rates apply to income for single filers, married couples filing jointly, heads of household, and married filing separately.

However, the income thresholds that determine which tax bracket your income falls into have shifted upward for 2026 — mainly due to inflation adjustments. In plain terms: the same dollar of income often needs to be higher in 2026 than in 2025 to reach a higher tax rate.

Here’s a visual comparison of the 2025 and 2026 tax brackets for single and married joint filers (selected brackets shown):

2025 Tax Year (reported 2026)

🔗 Learn more: 2025 tax rates

2026 Tax Year (reported 2027)

✔ In short: The income thresholds are higher for virtually every bracket in 2026 — meaning taxpayers can earn more before moving into a higher tax rate.

🔗 Learn more: 2026 tax rates

Understanding brackets is easier with examples.

Assume taxable income of $75,000.

In both 2025 and 2026, this taxpayer would fall within the middle brackets. However, because 2026 thresholds are higher, slightly more income may remain taxed at lower marginal rates before reaching the next tier.

Impact: Potentially lower overall tax compared to if thresholds had remained unchanged.

Assume taxable income of $180,000.

With higher 2026 thresholds, more of that income stays within lower brackets before progressing upward.

Impact: Improved tax efficiency and greater flexibility in income planning.

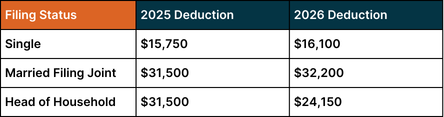

Standard deduction amounts also increased modestly for 2026:

🛡️ Roughly speaking, this means a slightly larger portion of income is shielded from federal tax for many taxpayers in 2026.

Because thresholds are inflation-adjusted, taxpayers are less likely to be bumped into a higher bracket simply due to cost-of-living wage increases. This helps preserve take-home pay — especially for middle-income clients.

Clients expecting a raise in 2026 should still estimate their tax outcome early — but these threshold increases may postpone marginal rate jumps. Tax planning tools that stress test income scenarios can quantify how much more clients can earn before crossing into higher brackets.

With the standard deduction rising, it may be preferable for some taxpayers to take the standard deduction instead of itemizing, especially if itemized deductions don’t exceed the higher 2026 amounts. A planner should review deductions such as mortgage interest, charitable gifts, and state taxes for itemization decisions.

With bracket thresholds adjusted, clients may need updated withholding so that they don’t underpay or overpay during the year.

If a client is near the top of a bracket in 2026, look at timing bonuses or self-employment income — possibly deferring income to 2027 when bracket thresholds could be even higher.

Contributing more to a 401(k) or IRA reduces taxable income and can help clients stay in a lower tax bracket. Retirement account limits also rose for 2026, supporting this strategy.

Capital gains tax thresholds were also updated for 2026. For investors near the top of capital gain brackets, timing the sale of long-term holdings can reduce tax liability.

Given the complexity and new legislative changes (like the One Big Beautiful Bill provisions affecting deductions and credits), working with a CPA or tax advisor can ensure clients get all eligible benefits.

Use this as a client-facing action list:

☐ Review W-4 withholding to reflect updated brackets

☐ Adjust quarterly estimated tax payments if self-employed

☐ Maximize retirement contributions (401(k), IRA, etc.)

☐ Evaluate whether to itemize or take the standard deduction

☐ Consider timing of bonuses or business income

☐ Review capital gains realization strategy

☐ Conduct a mid-year tax projection

✅ This transforms the conversation from reactive filing to proactive planning.

Truth: Only the income within that bracket is taxed at the higher rate. The U.S. uses a marginal tax system.

Truth: The tax rates stayed the same in 2026. Only income thresholds were adjusted for inflation.

Truth: With inflation adjustments and strategic deductions, taxpayers may maintain or even reduce effective tax rates.

Benefit from reduced risk of bracket creep.

Gain flexibility in timing income and deductible expenses.

Can strategically manage capital gains realization.

May benefit from improved withdrawal planning and bracket coordination with Social Security income.

Because thresholds increased, advisors and taxpayers should consider:

If near the top of a bracket, evaluate whether to defer income to the next tax year.

Higher limits in 2026 allow greater pre-tax savings, lowering taxable income.

Coordinate asset sales to optimize long-term capital gains exposure.

Run tax estimates mid-year to avoid surprises and optimize bracket positioning.

Tax brackets are only one part of the equation. A comprehensive 2026 strategy should also include:

🧩 Tax efficiency is not just about rates — it’s about coordination.

The 2026 tax updates reflect:

For most taxpayers, this creates a smoother transition and additional planning flexibility.

While the percentages remain unchanged, the increased income thresholds present meaningful strategic opportunities.

No. The seven federal income tax rates (10%, 12%, 22%, 24%, 32%, 35%, and 37%) remained the same. However, the income thresholds for each bracket were adjusted for inflation in 2026.

The IRS adjusts tax brackets annually to account for inflation. This helps prevent “bracket creep,” where taxpayers move into higher tax brackets simply because of cost-of-living increases.

Most taxpayers may be able to earn slightly more income before moving into a higher tax bracket. This could result in lower overall tax liability compared to if the brackets had not been adjusted.

Yes. The standard deduction increased in 2026, which means a larger portion of income is not subject to federal income tax for many filers.

Consider reviewing withholding, maximizing retirement contributions, timing income and deductions strategically, and consulting a tax professional to ensure you’re taking advantage of updated brackets and deductions.

Being audited is comparable to being struck by lightning. You don't want to practice pole vaulting in a thunderstorm just because it's unlikely. Making sure your books are accurate and your taxes are filed on time is one of the best ways to keep your head down during tax season. Check out Vincere's take on tax season!

This post is just for informational purposes and is not meant to be legal, business, or tax advice. Regarding the matters discussed in this post, each individual should consult his or her own attorney, business advisor, or tax advisor. Vincere accepts no responsibility for actions taken in reliance on the information contained in this document.

For business tax planning articles, our tax resources provides valuable insights into how you can reduce your tax liability now, and in the future.

.png)

At Vincere Tax, we've got the skills and know-how to craft a unique, tailored plan just for you. Trust us – we've got the expertise to make it happen!

Speak with an expert Website Terms.png)

.png)

.png)

Copyright © 2025 Vincere Tax| All Rights Reserved

Privacy Policy