Discover how cost segregation works, including 100% bonus depreciation rules, tax strategies, examples, and risks. Learn how to turn real estate into a powerful, numbers-driven wealth engine.

.png)

Real estate has long been considered one of the most effective vehicles for building wealth. Appreciation, leverage, and cash flow all play a role—but one of the most powerful and often misunderstood drivers of real estate wealth is taxation.

📊 Cost segregation sits at the center of that advantage.

Done correctly, it transforms a static tax deduction into a dynamic, front-loaded cash flow engine. Done poorly—or without strategy—it becomes a missed opportunity or even a liability.

In 2026, with the return of permanent 100% bonus depreciation, cost segregation is no longer just a niche tactic. It is a core planning tool for investors who want to align tax strategy with long-term wealth creation.

This guide breaks down exactly how it works, why it matters now more than ever, and how to use it as a numbers-driven wealth engine—not a one-time tax trick.

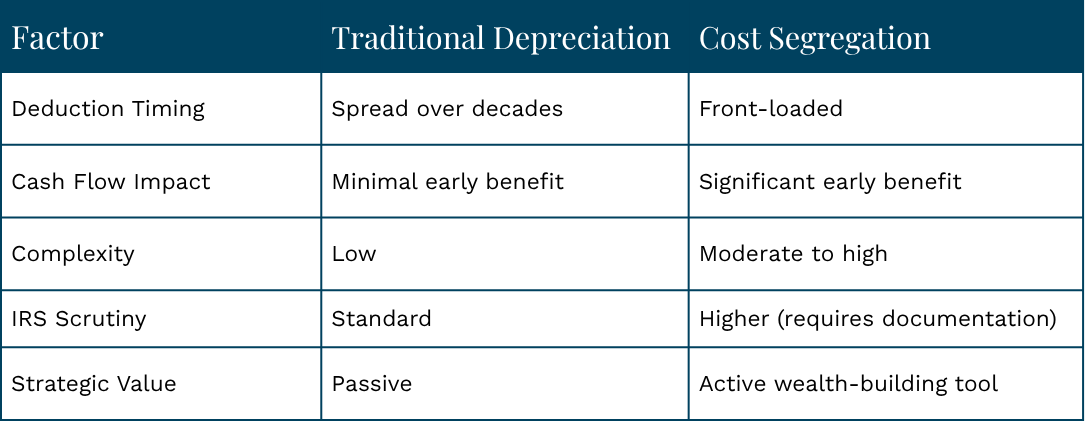

At its core, cost segregation is a tax strategy that accelerates depreciation.

Under standard rules, real estate is depreciated slowly:

This means investors typically recover their property cost gradually over decades.

Instead of treating a building as one asset, it breaks the property into individual components—each with its own depreciation schedule.

Examples include:

Many of these qualify for shorter depreciation lives:

💰 The result? Faster deductions and significantly improved early-year cash flow.

The biggest development shaping cost segregation today is the restoration of 100% bonus depreciation.

Under legislation passed in 2025, qualifying property placed in service after January 19, 2025 can be fully expensed in the first year.

If a cost segregation study reclassifies parts of a property into shorter-life assets:

For example:

Without cost segregation:

With cost segregation + bonus depreciation:

That difference is not theoretical—it directly impacts:

Cost segregation is often marketed as a tax-saving tool. That framing is incomplete. It is better understood as a cash flow acceleration system.

A dollar saved today is more valuable than a dollar saved later.

By accelerating depreciation:

Early tax savings can be reinvested into:

Over time, this creates a compounding effect that outpaces standard depreciation.

Many investors use cost segregation strategically to:

In practice, this can mean acquiring additional properties years earlier than otherwise possible.

A cost segregation study is not a spreadsheet exercise—it is an engineering-based analysis.

According to IRS guidance, these studies identify property components that qualify as shorter-life assets under depreciation rules.

Engineers review construction details, blueprints, and cost data

Components are categorized into appropriate depreciation classes

A formal report is created to support IRS compliance

Results are applied to depreciation schedules

📑 The IRS expects these studies to be detailed and defensible. Poor documentation increases audit risk.

Cost segregation is ultimately a math-driven strategy.

Typical outcomes:

Example:

This could generate:

🏠 These are not edge cases—they are common outcomes for qualifying properties.

Cost segregation is not universally beneficial. It is most effective when aligned with the right profile.

1. High-Income Investors

2. Large or Complex Properties

3. Long-Term Hold Investors

4. Real Estate Professionals

Without proper alignment, the strategy may underperform.

One of the most misunderstood aspects of cost segregation is how losses are used.

In most cases:

However:

This is where strategy matters more than the deduction itself.

Cost segregation is not “free money.” It accelerates deductions—but does not eliminate tax.

When a property is sold:

This creates a trade-off:

However, strategies like:

can mitigate or defer this impact.

Despite its benefits, cost segregation is not always the right move.

Common situations where it may fall short:

If you are not paying significant taxes, deductions provide limited value.

Selling quickly reduces the benefit of accelerated depreciation.

The cost of the study may outweigh the tax savings.

Passive loss limitations may delay benefits. As one real estate investor noted: “If you can’t use the loss… it just sits.”

This highlights a key truth: Cost segregation must fit your overall tax strategy—not just your property.

Cost segregation works best when integrated into a broader plan.

1. Acquisition Timing

2. Entity Structure

3. Exit Strategy

4. Income Forecasting

🧠 In 2026, the investors seeing the greatest success are not using cost segregation reactively—they are planning for it before closing.

Cost segregation should be part of a multi-year strategy.

Improper classification increases audit risk.

Deductions without usability create no real benefit.

ROI should be calculated before implementation.

The 2026 landscape reflects a shift:

This means:

📈 Cost segregation is evolving from a niche strategy into a standard component of sophisticated real estate investing.

Cost segregation is not about saving taxes. It is about controlling timing.

By accelerating depreciation, investors:

But the real power lies in coordination:

In 2026, the difference between average investors and high-performing ones is no longer access to strategies—it is execution.

🚀 Cost segregation, when used correctly, is not just a tax tool. It is a numbers-driven wealth engine.

Yes—more than ever due to permanent 100% bonus depreciation, allowing immediate expensing of qualifying assets.

Typically several thousand dollars, depending on property size and complexity.

Yes, as long as the property is used for income-producing purposes.

Not inherently, but poorly prepared studies can trigger scrutiny. Proper documentation is essential.

Depreciation recapture and inability to use losses effectively if not properly planned.

Being audited is comparable to being struck by lightning. You don't want to practice pole vaulting in a thunderstorm just because it's unlikely. Making sure your books are accurate and your taxes are filed on time is one of the best ways to keep your head down during tax season. Check out Vincere's take on tax season!

This post is just for informational purposes and is not meant to be legal, business, or tax advice. Regarding the matters discussed in this post, each individual should consult his or her own attorney, business advisor, or tax advisor. Vincere accepts no responsibility for actions taken in reliance on the information contained in this document.

For business tax planning articles, our tax resources provides valuable insights into how you can reduce your tax liability now, and in the future.

.png)

At Vincere Tax, we've got the skills and know-how to craft a unique, tailored plan just for you. Trust us – we've got the expertise to make it happen!

Speak with an expert Website Terms.png)

.png)

.png)

Copyright © 2025 Vincere Tax| All Rights Reserved

Privacy Policy